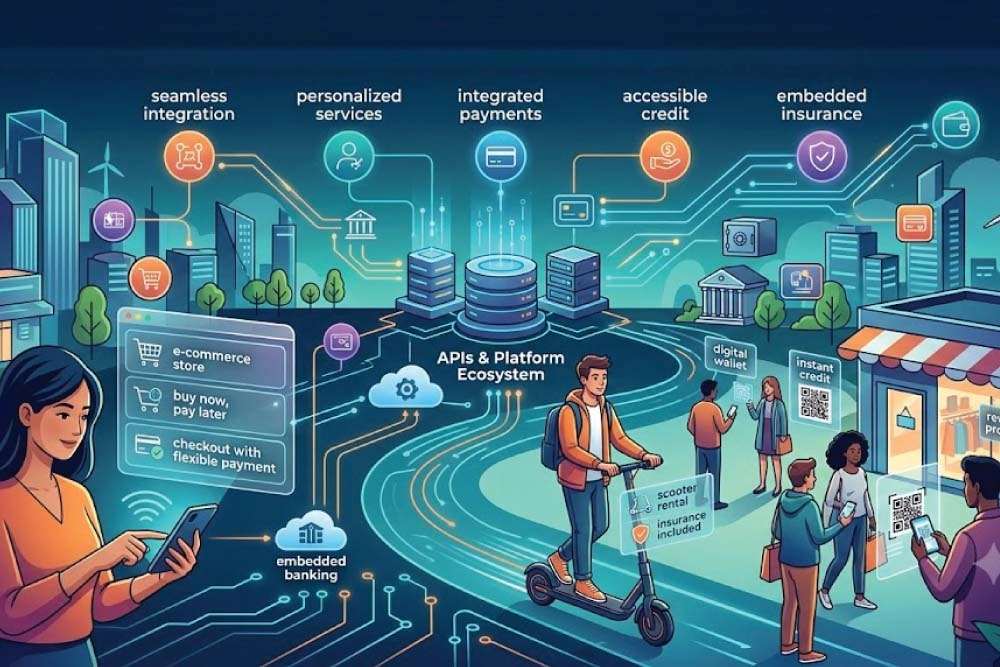

Financial services are no longer confined to banks, credit unions, or traditional financial institutions. A new era of commerce is emerging in which financial products and services are seamlessly integrated into everyday consumer experiences. This phenomenon, known as embedded finance, is transforming the way individuals shop, pay, borrow, save, and invest.

From e-commerce platforms offering instant credit at checkout to ride-hailing apps providing digital wallets and insurance products, embedded finance is rapidly becoming a cornerstone of the modern consumer economy. As technology companies, retailers, and fintech firms continue to innovate, the lines between commerce and finance are increasingly disappearing.

For businesses, embedded finance presents an opportunity to deepen customer relationships and create new revenue streams. For consumers, it offers greater convenience, accessibility, and personalization.

Instead of being redirected to a bank or third-party provider, consumers can access financial products within the platforms they already use.

Examples include:

- Buy Now, Pay Later (BNPL) options during online purchases

- Digital wallets integrated into retail applications

- Insurance products offered during travel bookings

- Small business financing embedded within e-commerce marketplaces

- Instant payment solutions available through mobile apps

This seamless integration removes friction from financial transactions and enhances the overall customer experience.

Why Consumers Are Embracing Embedded Finance

Modern consumers prioritize convenience. They expect fast, intuitive, and personalized digital experiences across all aspects of their lives. Embedded finance addresses these expectations by simplifying financial interactions.

Consumers increasingly prefer financial services that fit naturally into their daily activities. Rather than navigating multiple platforms, users can access payment solutions, financing options, and financial tools within a single ecosystem.

The rise of digital-native generations has further accelerated adoption. Younger consumers are particularly comfortable using technology-driven financial solutions and often prioritize user experience over traditional banking relationships.

As a result, embedded finance is becoming an important driver of customer loyalty and engagement.

Retail and E-Commerce Are Leading the Way

The retail industry has emerged as one of the strongest adopters of embedded finance solutions. Retailers are using financial services not only to facilitate transactions but also to enhance customer retention and increase sales.

Buy Now, Pay Later services have become a popular feature in e-commerce, allowing consumers to spread payments over time without the complexity of traditional credit applications. This flexibility often encourages higher spending while improving conversion rates for merchants.

Digital wallets, loyalty programs, and personalized financing options are also helping retailers create more integrated customer journeys. These services provide valuable consumer insights while improving convenience and satisfaction.

As competition intensifies, embedded finance is becoming a strategic differentiator for retailers seeking to strengthen customer relationships.

FinTech Innovation Is Driving Growth

FinTech companies play a critical role in the expansion of embedded finance. Through APIs, cloud-based platforms, and Banking-as-a-Service solutions, fintech providers enable businesses to offer financial products without becoming full-scale financial institutions.

This infrastructure allows companies across industries to integrate payments, lending, insurance, and investment products quickly and efficiently. As technology becomes more sophisticated, businesses can launch customized financial solutions with lower costs and faster implementation timelines.

The growing collaboration between banks and fintech firms is creating a more dynamic financial ecosystem that benefits both businesses and consumers.

Data and Personalization as Competitive Advantages

One of the most significant strengths of embedded finance lies in its ability to leverage customer data. Businesses can analyze purchasing behaviour, spending patterns, and engagement metrics to deliver highly personalized financial offerings.

For example, a retailer may offer installment payment plans based on a customer’s purchasing history, while a digital marketplace may provide tailored financing options to sellers based on transaction data.

This personalization improves customer experiences while increasing the likelihood of product adoption. Companies that effectively utilize data-driven insights are gaining a competitive advantage in an increasingly crowded marketplace.

However, the growing use of consumer data also raises important considerations around privacy, security, and regulatory compliance.

Challenges Facing the Industry

Despite its rapid growth, embedded finance faces several challenges. Regulatory requirements continue to evolve as governments seek to balance innovation with consumer protection. Companies must ensure compliance while maintaining seamless user experiences.

Cybersecurity remains another major concern. As financial services become integrated into more digital platforms, organizations must invest heavily in security infrastructure to protect sensitive customer information.

Additionally, businesses must carefully manage customer trust. Transparency regarding fees, terms, and financial obligations is essential to maintaining credibility and long-term relationships.

Organizations that prioritize security, compliance, and ethical practices will be better positioned for sustainable growth.

The Future of Embedded Finance

The future of embedded finance extends far beyond payments and lending. Advances in artificial intelligence, open banking, and digital identity technologies are expected to unlock new opportunities across industries.

Financial services will become increasingly contextual, appearing exactly when and where consumers need them. Whether purchasing products, booking travel, managing subscriptions, or operating businesses, consumers will encounter financial solutions seamlessly integrated into their digital experiences.

As adoption continues to grow, embedded finance is expected to become a fundamental component of the global digital economy.

Embedded finance is reshaping the relationship between consumers, businesses, and financial services. By integrating financial products directly into everyday experiences, organizations are creating more convenient, personalized, and accessible solutions.

The convergence of technology, commerce, and finance is generating new opportunities for innovation while redefining consumer expectations. Businesses that embrace embedded finance strategically will not only enhance customer experiences but also position themselves at the forefront of the evolving digital economy.

In the years ahead, embedded finance will move from being a competitive advantage to becoming an essential element of modern business strategy.